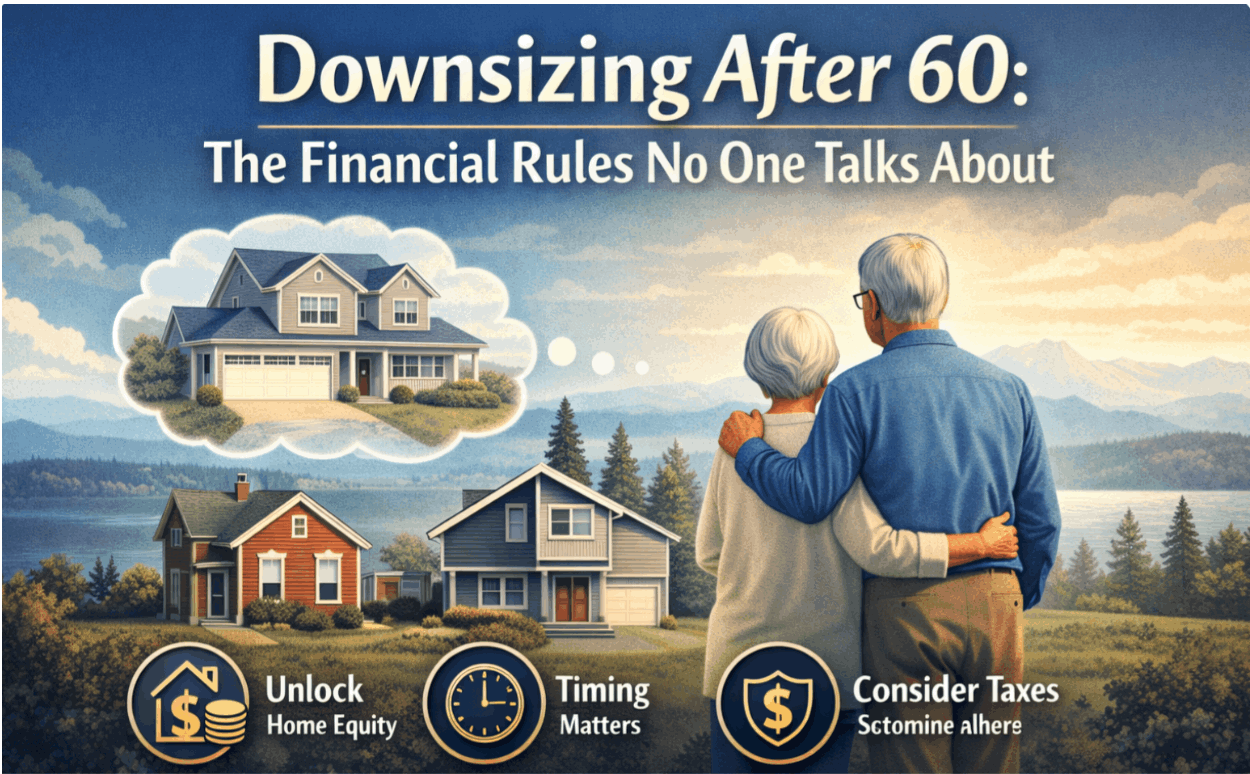

Downsizing After 60: The Financial Rules No One Talks About

For many homeowners, the idea of downsizing after 60 sounds simple. Sell the larger home, move into something smaller, and enjoy a more manageable lifestyle.

For many homeowners, the idea of downsizing after 60 sounds simple. Sell the larger home, move into something smaller, and enjoy a more manageable lifestyle.

In reality, downsizing is often one of the most important financial decisions homeowners make in retirement.

Understanding the financial rules that come with downsizing can help homeowners make smarter decisions and avoid unexpected surprises.

Rule #1: Your Home May Be Your Largest Retirement Asset

For many people approaching retirement, their home represents the largest portion of their net worth.

Decades of mortgage payments, appreciation, and market growth have created significant equity. Downsizing can unlock that equity and allow homeowners to redirect those funds toward retirement income, investments, travel, or helping family members.

However, accessing that equity requires thoughtful planning.

Rule #2: Smaller Homes Often Cost More Per Square Foot

One of the most surprising realities of downsizing is that smaller homes often have a higher price per square foot than larger homes.

Condos and townhomes may also include HOA dues that cover maintenance, insurance, landscaping, and amenities.

While these services provide convenience, they can increase monthly housing costs if not considered carefully.

Rule #3: Maintenance Costs Matter More Than Size

Downsizing is often motivated by the desire to reduce maintenance responsibilities.

However, choosing the right property is key.

Homes with fewer stairs, smaller yards, and updated systems can reduce long-term maintenance costs and improve day-to-day comfort.

Rule #4: Timing the Move Creates More Options

Many homeowners wait too long to downsize.

The best outcomes often occur when people begin planning before a move becomes urgent due to health, financial changes, or family needs.

Planning ahead allows homeowners to explore communities, evaluate housing options, and make thoughtful financial decisions.

Rule #5: Tax Rules Can Protect Your Equity

The IRS allows homeowners to exclude up to:

- $250,000 in capital gains (single)

- $500,000 in capital gains (married couples)

When selling a primary residence, provided ownership and residency requirements are met.

Understanding this rule can help homeowners preserve more of the equity they’ve built over time.

Downsizing Is About Lifestyle, Not Just Square Footage

Ultimately, downsizing is not simply about moving into a smaller home.

It is about designing the next chapter of life.

For some homeowners, that means relocating closer to family. For others, it means living in a walkable neighborhood, reducing maintenance responsibilities, or freeing up financial resources for travel and experiences.

The most successful downsizing transitions begin with thoughtful planning and professional guidance.

When homeowners approach the process strategically, downsizing can create greater financial freedom and a lifestyle that better supports their goals.

Categories

Recent Posts

GET MORE INFORMATION